Written Commentary

CORN

Prices were $.01-$.02 lower in choppy 2 sided trade. Spreads firmed a touch despite a 5th consecutive lower close. Next support for spot July is at $3.99, the low from last fall on the weekly chart. Dec-25 carved out a new contract low. Exports sale at 41 mil. bu. were in line with expectations. Old crop commitments at 2.660 bil. are up 27% from YA, vs. the USDA forecast of up 16%. Current commitments represent just over 100% of the USDA forecast vs. the historical average of 95%. New crop exports in the July WASDE will likely hinge on how aggressive the USDA raises Brazil’s 24/25 production. The European Commission increased their 25/26 production forecast .8 mmt to 64.6 mmt however held their import forecast unchanged at 18.3 mmt. These estimates compare to the USDA 60 mmt and 20.5 mmt respectively. Datagro increased their 24/25 Brazilian corn production forecast 1.3 mmt to 134 mmt, above the USDA forecast of 130 mmt, however well below the AgroConsults est. of 150 mmt. The BAGE estimates Argentine harvest has reached 55%, up 6% for the week. While citing strong yield they kept their production forecast unchanged at 49 mmt vs. the USDA at 50 mmt.

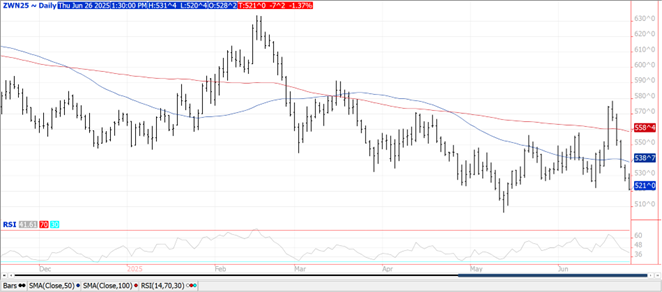

SOYBEANS

Prices are mixed with beans down $.02-$.03, meal was off another $4-$5 while oil rebounded 55-75 points. Bean spreads were mixed, oil spreads firmed while meal spreads slipped to new lows. Nov-25 beans slipped to new monthly low while holding support just above the May low. July-25 oil narrowed the gap from last Monday’s limit up trade before recovering. New contract low for July-25 meal for a 5th consecutive session with the spot contract falling to a fresh 9 year low. Spot board crush margins slipped $.01 to $1.51 with bean oil PV surging back above 49%. New crop margins were steady at $1.96 ½. Precipitation maps show rainfall totals continue to stack up in the NW third of the corn and soybean belt. Rains thru early next week will continue to favor the NC Midwest, lighter amounts for the ECB, and even lighter amounts for the far WCB. Extended forecasts thru the 1st full week of July show the above normal precipitation and normal temperatures across the nation’s midsection. Soybean sales at 21 mil. bu. were in line with expectations. Old crop commitments at 1.818 bil. are up 11% from YA vs. the USDA forecast of up 9%. As expected no sales to China. Soybean meal sales at 260k tons were in line with expectations. YTD commitments are up 11% from YA, vs. USDA up 8%. Bean oil sales at 4k tons (8.8 mil. lbs) were in line with expectations. YTD commitments at 2.328 bil. lbs. represent 90% of the USDA forecast.

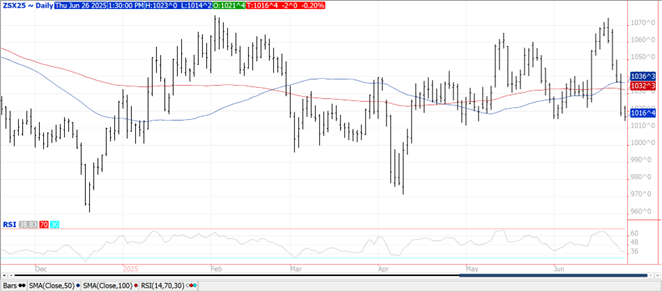

WHEAT

Prices ranged from $.04-$.07 lower across the 3 classes. Spreads are mixed. All 3 classes violated support at their June lows. This week’s updated drought monitor show drought conditions ease for corn and soybean acres, while turning higher for spring and winter wheat. Export sales at 9 mil. bu. were below expectations. YTD commitments at 242 mil. bu. are up 8% from YA, vs. the USDA forecast of up 1%. Commitments represent 29% of the USDA forecast, above the historical average of 27%. Global wheat buyers backed away from US as prices spiked earlier this month. IKAR raised their Russian wheat production forecast 700k mt to 84.5 mmt, just above both the USDA and SovEcon who are at 83 mmt. The IGC raised their global wheat production forecast for 25/26 2 mmt to 808 mmt, consistent with the USDA at 808.6. The European Commission increased their soft wheat production forecast 1.6 mmt to 128.2 mmt while holding their export forecast unchanged at 29.8 mmt. The BAGE reports Argentine plantings advanced 12% LW to 73% complete.

Charts provided by QST.

>>See more market commentary here.

Risk Warning: Investments in Equities, Contracts for Difference (CFDs) in any instrument, Futures, Options, Derivatives and Foreign Exchange can fluctuate in value. Investors should therefore be aware that they may not realise the initial amount invested and may incur additional liabilities. These investments may be subject to above average financial risk of loss. Investors should consider their financial circumstances, investment experience and if it is appropriate to invest. If necessary, seek independent financial advice.

ADM Investor Services International Limited, registered in England No. 2547805, is authorised and regulated by the Financial Conduct Authority [FRN 148474] and is a member of the London Stock Exchange. Registered office: 3rd Floor, The Minster Building, 21 Mincing Lane, London EC3R 7AG.

A subsidiary of Archer Daniels Midland Company.

© 2021 ADM Investor Services International Limited.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.