Written Commentary

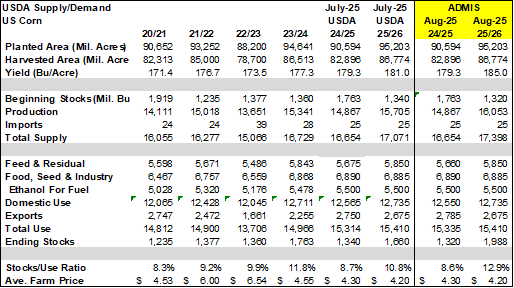

CORN

Prices were $.04-$.06 higher closing near session highs. Although Sept/Dec spread eased to a new low, new crop spreads firmed. Today was the first day of the Goldman roll. Next resistance for Dec-25 is this week’s high at $4.12 ¾. Exports at 131 mil. bu. (124 mil.–25/26 MY) were above expectations. Old crop commitments at 2.780 bil. are up 27% from YA, vs. the USDA forecast of up 22%. New crop commitments surged to 464 mil. more than double the YA pace and the highest in 4 years. New crop buyers were spread out with unknown buying 50 mil. Mexico and Japan with 16 mil. each, 13 mil. to Colombia and 12 mil. to Japan. In addition the USDA announced new crop sales of 4 mil. bu. to both Mexico and Guatemala. Expana (formerly Strategies Grain) lowered their EU production forecast by 1.5 mmt to 54.8 mmt, well below the USDA forecast of 60 mmt. Brazil’s Ag. Ministry reports they exported 2.434 mmt of corn in July, down 31.5% YOY.

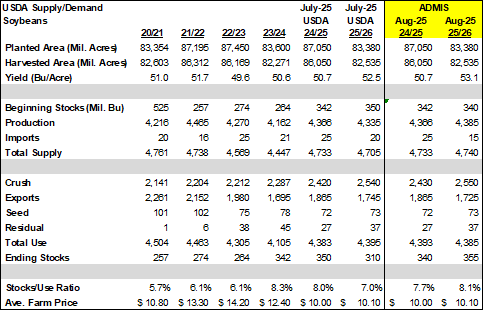

SOYBEANS

Prices were mixed with beans $.08-$.10 higher, meal was up $3-$4 while bean oil backed up another 15-20 points. Bean spreads were mixed while product spreads eased. Inside trade for both Sept-25 and Nov-25 beans. Sept-25 bean oil traded below the previous sessions low for 6 consecutive sessions. Next support is the 50 day MA at 52.81. Inside trade for Sept-25 meal. Much above normal temperatures across the S. plains and WCB will gradually ease to more normal readings by early next. Except for the NC Midwest and ND much of the Midwest will experience net drying over the next week. Some late season crop stress is likely. Additional rains the 2nd half of August will be needed to maximize yield potential. Spot board crush margins slipped $.01 to $2.22 bu. while bean oil PV pulled back to 49.2%. Chinese census data showed they imported 11.67 mmt of soybeans in July-25. While down from 12.264 mmt in June-25 they were above expectations and well above the 9.85 mmt in July-24. Their YTD imports at just over 61 mmt are up 4.6% YOY. Roughly 9.6 mmt of China’s imports came from Brazil in July. Brazil’s Ag. Ministry reports their total exports in July were 12.26 mmt, up 9% YOY. US exports at 37 mil. bu. last week were at the high end of expectations. Old crop commitments at 1.892 bil. are up 13% from YA vs. the USDA forecast of up 10%. New crop commitments jumped to 132 mil. bu. still down 21% YOY and represent only 7.5% of the USDA forecast, vs. the historical average of 20%. Still no new crop sales on the books to China. Soybean meal sales at 281k tons were in line with expectations. Old crop commitments are up 13% from YA, vs. USDA up 8%. Bean oil sales at 7k tons (15.4 mil. lbs) were in line with expectations.

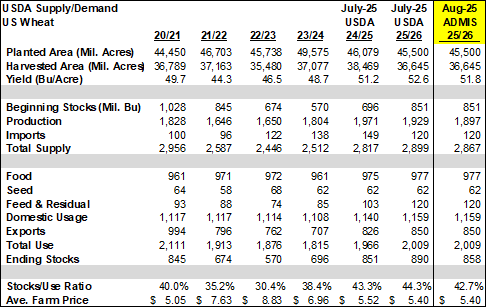

WHEAT

Prices ranged from $.05-$.10 higher across the 3 classes. Sept-25 MIAX futures established a key reversal day. Tunisia reportedly purchased 75k mt of soft wheat at an average price of just over $262.50/mt CF. A Korean feed mill reportedly bought 65k mt of US feed wheat just below $263/mt CF. Expana raised their EU 25/26 soft wheat production forecast 2.1 mmt to 132.8 mmt. Exports at 27 mil. bu. were above expectations. YTD commitments at 378 mil. bu. are the highest in 5 years and up 21% from YA, vs. the USDA forecast of up 3%. YTD by class sales vs. the USDA forecast are HRW up 96% vs. USDA up 26%, SRW up 15% vs. USDA up 3%, HRS down 4% in line with USDA, and white down 17% vs. down 14%.

Charts provided by QST.

Risk Warning: Investments in Equities, Contracts for Difference (CFDs) in any instrument, Futures, Options, Derivatives and Foreign Exchange can fluctuate in value. Investors should therefore be aware that they may not realise the initial amount invested and may incur additional liabilities. These investments may be subject to above average financial risk of loss. Investors should consider their financial circumstances, investment experience and if it is appropriate to invest. If necessary, seek independent financial advice.

ADM Investor Services International Limited, registered in England No. 2547805, is authorised and regulated by the Financial Conduct Authority [FRN 148474] and is a member of the London Stock Exchange. Registered office: 3rd Floor, The Minster Building, 21 Mincing Lane, London EC3R 7AG.

A subsidiary of Archer Daniels Midland Company.

© 2021 ADM Investor Services International Limited.

Futures and options trading involve significant risk of loss and may not be suitable for everyone. Therefore, carefully consider whether such trading is suitable for you in light of your financial condition. The information and comments contained herein is provided by ADMIS and in no way should be construed to be information provided by ADM. The author of this report did not have a financial interest in any of the contracts discussed in this report at the time the report was prepared. The information provided is designed to assist in your analysis and evaluation of the futures and options markets. However, any decisions you may make to buy, sell or hold a futures or options position on such research are entirely your own and not in any way deemed to be endorsed by or attributed to ADMIS. Copyright ADM Investor Services, Inc.